Why superfan subscriptions are dying out

Lessons from Vault, Patreon, and Spotify.

Hi there!

With the transition into May, music industry conference season is officially underway. Here’s my speaking itinerary for the next few months; if we’ll be in the same place at the same time, please reach out.

🚨 If you’ll be in NYC next week, Seth Hillinger and I are hosting ~music rizz~, a casual pre-conference checkpoint for the local music-tech community before Music Biz, Amplify, Indie Week, and the rest of the season kick in. Expect a more interactive format than the usual mixer, with structured ways to meet people you don't already know, share what you're working on, and surface what you're looking for next. This event is free to attend with approval; capacity is limited, so we will be hand-curating the attendee list. You can RSVP here.

I’ve been writing a lot about AI music recently :) So today’s article takes a different direction — looking at why superfan subscriptions are quietly dying out across the industry, and the new paradigm of fan platforms that are replacing them.

We’ve had 200 new subscribers join us since the last issue. If you’re one of these folks, welcome! Feel free to reply directly to this email to introduce yourself — I read everything that comes through.

Thank you so much for your support!

Best,

Cherie Hu

Founder, Water & Music

Why superfan subscriptions are dying out

You can also read this article via our newsletter archives or on LinkedIn.

I.

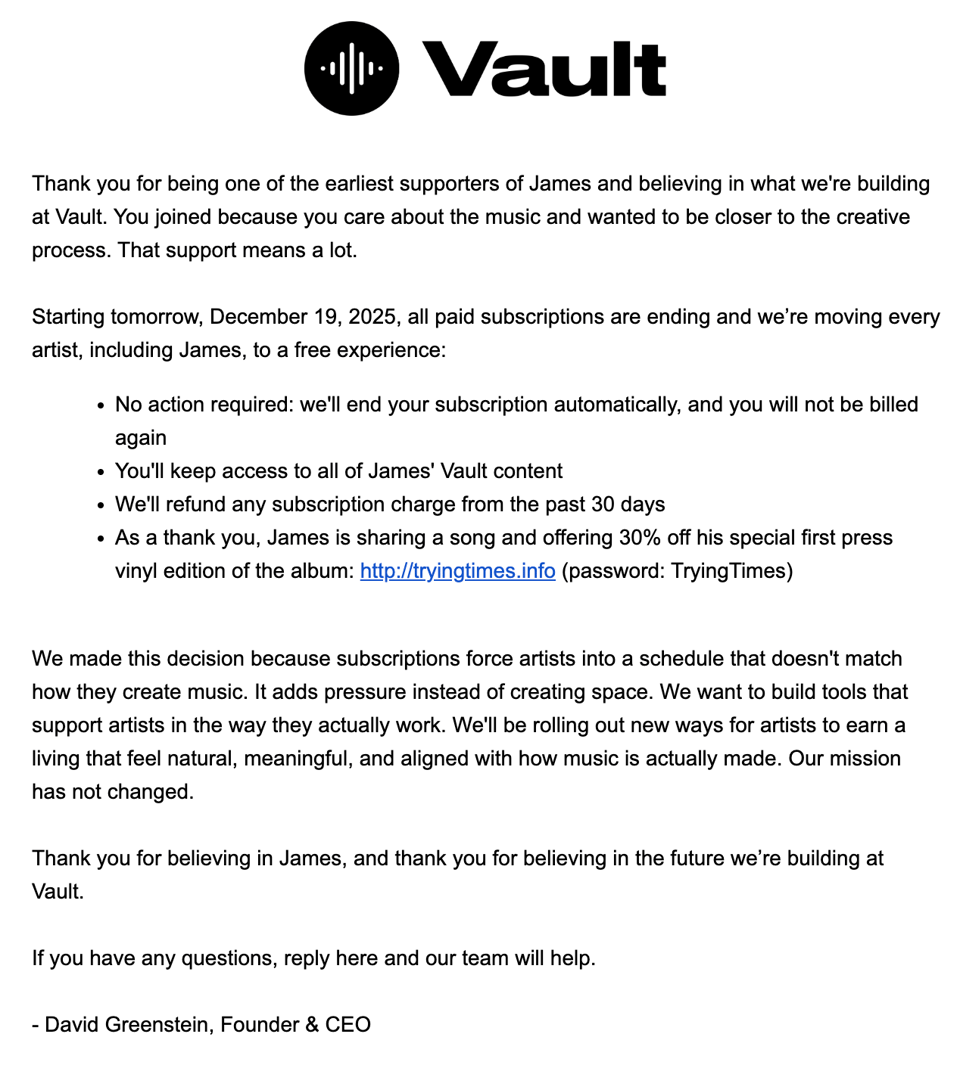

On December 19, 2025, Vault — the direct-to-fan subscription service that James Blake popularized as an antidote to streaming — quietly removed subscriptions from its business model.

In March 2024, Blake had partnered with Vault to launch his own subscription as an “experiment” beyond the low-margin economics of streaming. Fans could pay Blake $5/month to access unreleased tracks and demos, plus a private group chat with the artist and fellow subscribers.

As I wrote at the time, Blake was one of the best possible test cases for the direct artist subscription model. He had spent years in major-label limbo, so his critique of streaming and the surrounding industry machine had real stakes. He also had a loyal fan base likely to value what he was offering, namely unfiltered snapshots of his creative process.

To his credit, Blake was genuinely engaged on the platform. He dropped new tracks almost weekly, participated actively in his group chat, and gave subscribers perks like first access to private IRL shows.

“The concept of subscribing to an artist directly, I think can change the game and release artists from the relentless merry-go-round of the current state of things,” Blake wrote on X at the time of launch. “This is hopefully a great step towards allowing artists to be as authentic as possible, while still making a living.”

Vault slowly expanded its roster, launching other paid subscriptions with artists like Memba and Emily Bear. But none were able to generate the same momentum. Ultimately, the company concluded that direct-to-fan subscriptions were hard to scale and created the wrong incentives for artists.

On December 18, 2025, with one day’s notice, Vault Founder & CEO David Greenstein emailed Blake’s paid subscribers to announce that they would be moved to a “free experience,” with all existing Vault content and direct messaging still intact. Greenstein’s explanation for the transition was refreshingly blunt:

“We made this decision because subscriptions force artists into a schedule that doesn't match how they create music. It adds pressure instead of creating space. We want to build tools that support artists in the way they actually work."

Judging by its current homepage, Vault has repositioned itself as a broader direct-to-fan platform, with drops, digital music sales, SMS and email marketing, and fan analytics combined into one interface. Other artists using Vault for direct-to-fan communications today include Kesha, Nicole Moudaber, Lyrah, and JEV. There is no paid subscription offer in sight.

Vault’s move away from subscriptions appears to have gone unreported by the press, which is striking given the initial hype around its launch and Blake’s endorsement. I think that silence is part of a wider pattern: Music’s default reference points for “superfan subscriptions” are quietly backing away from the vision they helped establish.

II.

Much of the last five years of “superfan” hype traces back to COVID, which created a perfect storm of demand for direct-to-fan experiences. The collapse of touring left artists looking for recurring digital income, while fans no longer spending on IRL shows could redirect some of that money online.

One of the biggest beneficiaries was Patreon, which has lived most of its 13-year existence as a paid membership platform for creative professionals, including musicians, writers, podcasters, vloggers, and illustrators.

During early COVID, music on Patreon — previously more of a secondary, underdog category — quickly became one of the platform’s fastest-growing revenue sources. Between March and May 2020, the collective value that fans were paying musicians on Patreon increased by over 60%, while the total number of musician accounts on the platform increased by 200%, as I reported at the time. More broadly, the normalization of direct patronage helped Patreon’s valuation grow more than 3x in less than a year, from $1.2B in September 2020 to $4B in April 2021.

This would ultimately prove to be a bubble that inflated expectations around the long-term durability of fan patronage. As the pandemic subsided, subscription fatigue set in, and people returned to their normal routines, Patreon took a financial hit, laying off 17% of its staff in late 2022.

Today, paid memberships are no longer central to how Patreon positions itself online. It takes more than 30 seconds of reading their new homepage to find the word ”membership,” in tiny text near the bottom. The copy that shows up beforehand paints a portrait of creative communities with much broader strokes, emphasizing features like direct messages, group chats, and email outreach that are free by default for fans to access. If there is any discussion about paid offerings, it is more about digital shops where fans can make one-time payments for individual podcasts, videos, songs, or other kinds of content, rather than about recurring memberships.

This is not only a new brand for Patreon, but also a new business model. Free memberships first became available on Patreon in 2023; there are now 4x more free memberships than paid memberships on the platform (100 million vs. 25 million, respectively). As of December 2025, Patreon's one-time payments product was growing 3x faster than paid memberships. The focus now seems to be on building a wide freemium funnel upfront, with multiple monetization paths for fans to follow when the offering and timing are right.

All of this should not lead to the conclusion that Patreon “failed” in music. Music-related memberships are still alive and well: According to third-party analytics site Graphtreon, the top 10 music creators on Patreon have nearly 100,000 paid members combined.

But these top accounts are almost all music educators, reviewers, or commentators — roles better suited to paid membership than the traditional recording artist.

With education, teaching has a natural, recurring cadence; with reviews, there's always new music (and new industry goss) to discuss and react to. In contrast, recording and touring artists' careers are much more “spiky.” They might spend months or years writing and recording, then months or years promoting and performing, then disappear to reflect, explore, or recover before returning again to the public.

The moments when an artist might want to show up and engage with fans — releases, tours, anniversaries, reunions, archival drops, scandals, emotional live events — are not evenly distributed. Extended silence is often an intentional part of the work. Trying to fit this rhythm into a recurring software subscription or membership model is challenging for the majority of artists, and in most cases just gives those artists and their teams more work to do. A healthier question might be what better economics look like around the work they’re already doing.

The same is true on the fan side. There is no single definition of a fan. If we think of a fan as someone whose attention, identity, social life, taste, or spending repeatedly orients around an artist and their work, we quickly see how diverse that can look in practice. Sometimes that support is financial; sometimes it is promotional; sometimes it is emotional; often, it is all three.

The many behaviors that shape this fandom — across streaming, buying tickets, traveling for shows, collecting vinyl, joining a Discord, watching livestreams, reposting clips — each have their own timing and internal logic. Across these formats, a fan might spend $150 in one week, then nothing for the next six months. That does not make them less valuable — in fact, it makes them normal! They want to feel close to the artist at the right moment, not necessarily every first Tuesday.

The problem with direct artist subscriptions is that they flatten all this activity into one signal: Did you pay this month? An emotional relationship turns into a quiet obligation. Like any discerning consumer, the fan starts asking whether they are getting “enough” “content” to justify the charge, and the artist starts wondering what they “owe.” I don’t think that’s the feeling anyone wanted to encourage here.

So for superfan subscription platforms, fan conversion stays narrow, artist churn is high, and attention fragments across multiple artists. Fans eventually grow tired of having a separate app, login, chat, and payment flow for every artist they love.

The deeper lesson for both Patreon and Vault is one that many other platforms are now confronting: A direct fan relationship in music cannot be reduced to a monthly bill.

One exception worth calling out: In April 2026, the Grateful Dead and nugs.net launched Play Dead, a subscription app for hi-res streaming of the band's live archive. Priced at $9.99/month or $99.99/year, the app debuted with hundreds of recordings, including 20 previously unreleased shows, and new vault releases continue to drop every Tuesday.

This is close to the ideal subscription use case. No current band members are being asked to produce weekly content; the product is the archive itself. Deadheads also have a long culture of collecting, comparing, and circulating variations of live recordings, where one song from one night is not interchangeable with the same song from another night. The subscription is not manufacturing a new behavior, but formalizing one that already existed.

III.

If superfan hype entered the public imagination in early COVID, it entered the boardroom in 2023.

For more than a decade, recorded music could point to subscriber growth as the answer to almost every anxiety. More paying users meant more revenue; more revenue meant more confidence. But by 2023, standard streaming had matured in many major markets, and family plans had trained listeners to expect shared access at lower prices. Average revenue per user (ARPU) on paid streaming has fallen more than 40% over the last 10 years.

At this saturation point, the industry needed a cleaner way to talk about future value growth — and “superfans” became the default language for articulating that vision. Whereas streaming rebuilt recorded music by standardizing access, now the industry wanted to reintroduce some notion of difference: different prices, products, and degrees of proximity for different fans.

Goldman’s 2023 “Music in the Air” report formalized the idea, calling “superfan segmentation” a potential $4B incremental revenue opportunity by 2030. That number became powerful, and appeared in dozens of pitch decks, because it sounded both large and orderly.

The critical caveat is that the scope of this $4B analysis is narrower than you might think. Goldman’s financial model focused only on streaming subscriptions, and assumed that 20% of current subscribers were “superfans” willing to pay $22.80/month for a premium streaming experience. In other words, the $4B number was not a full accounting of superfan spending across merch, ticketing, vinyl, travel, communities, and emotional labor. It was simply an argument that streaming should be more expensive for certain listeners.

One month later, Luminate gave the industry a broader, more culturally useful definition of “superfan” in its 2023 Midyear Music Report. Luminate estimated that 15% of the U.S. general public could be categorized as superfans — defined in this case as music listeners aged 13+ who engage with artists in five or more ways, including streaming, social media, merch, physical music, and live shows.

The gap between Goldman’s and Luminate’s definitions captures a core tension in the industry today: Superfans are whole people, whole human beings, but are often modeled simply as higher-paying streaming subscribers. That narrowing is appealing for obvious reasons: Recurring revenue is easier to forecast, investors understand it, and “higher ARPU from existing users” sounds cleaner than the messy reality of fan behavior.

Universal Music Group has been the major label most aggressive in absorbing superfan logic into its strategy. At its September 2024 Capital Markets Day, the company named “accelerating superfan monetization” as a key driver of its financial targets through 2028. Executives argued that streaming had flattened monetization across casual and intense listeners, leaving money on the table for direct-to-consumer revenue.

As of late 2024, UMG’s DTC vertical was growing at a 33% CAGR, making it one of the fastest-growing parts of their business and the clearest commercial expressions of what a superfan-centric strategy could look like. Across listening parties, virtual stores, Roblox activations, and investments in the likes of Weverse and Stationhead, “superfans” for UMG have been expanding beyond one-off community strategy, into an ARPU strategy and platform strategy that scales across the entire organization.

If Goldman and UMG have been describing this opportunity, the natural question follows: What is the world’s largest streaming service doing about it?

So far, Spotify’s answer has been a long public tease. By late 2024, Spotify was openly discussing a higher-priced tier with better sound quality and other features. In early 2025, Reuters reporting suggested a Music Pro add-on could cost up to $5.99 more per month and include higher-quality audio, AI-powered remixing tools, and access to concert tickets. Spotify kept talking around the product, but the exact contents of the bundle kept shifting. Then, in September 2025, lossless audio — previously framed as one of the cleanest possible upsell features — arrived inside standard Premium for everyone, instead of a separate super-premium tier.

Spotify’s latest Q1 2026 results were filled with new updates around features like Taste Profiles, Prompted Playlists, SongDNA, and invite-only live events for top fans. As far as the superfan tier goes, there has been no official update.

Bloomberg reported that Spotify has been unable to settle on the features that should be in such a plan. We can understand this as Spotify facing the institutional version of the superfan problem.

Spotify does not lack scale, listening data, or any reason to make more money per user. What it lacks is an obvious definition of what superfans should pay for inside a streaming app for mass-market consumers. Hi-fi audio, ticket access, and AI remixing each point to different user behaviors, infrastructure, and legal needs; combining all of those into a single interface risks creating a bloated, unfocused experience.

Ironically, this is the same problem Vault and Patreon faced with superfan subscriptions, but from the opposite direction. Vault and Patreon began with artist intimacy, then ran into the reality that many recording artists are not “creators” in the cadenced sense. Spotify began with consumption at global scale, and is running into the fact that the most valuable fan behaviors often happen somewhere else entirely.

IV.

What gives?

The story across Vault, Patreon, and Spotify is not that superfans are “over.” It is that the superfan subscription is losing its status as the default answer to how fans and artists should relate online.

The first principles still hold: Artists need better ways to earn outside the dilution of streaming payouts. Many fans want closer relationships with the artists they love, and will spend more when the offer feels right. Labels, managers, and platforms continue to look for more value from the listeners who care most. None of that has changed.

What has changed is the assumption that closeness should automatically become a monthly content bill. The subscription model imported a particular logic from software and creator media — predictable cadence, recurring deliverables, a steady drip of new material — and mapped it onto careers that have never worked that way. Artist behavior and fan behavior are rarely recurring in the way that superfan subscriptions require them to be.

The next generation of fan platforms — Laylo, Openstage, EVEN, Stationhead, Softside, Superfan, Medallion, b.stage, Weverse — is running on a different paradigm. Some are building around drops, SMS, and fan contact data; others are turning release campaigns, merch, listening parties, archives, fan-designed products, or concert histories into moments fans are already willing to pay around. The most important mindset shift is from “pay every month for access,” to: “be reachable, recognized, and ready when something meaningful happens.”

How these platforms will figure out the right shape for that work will be one of the most interesting trends to watch for the next few years. For now, we have our answer to the titular question: Superfan subscriptions are dying out because, for most artists, they are too narrow for the job. What replaces them will be less about exclusive clubs, and more about tools that match the irregular, high-intent ways that artistry and fandom already work. ★