Extended Play: Just how difficult is it to make a sustainable living from streaming?

Water & Music — The innovator's guide to the music business.

Today's date is September 27, 2021.

Thanks so much for being a paying Water & Music member.

Hello Reader,

Hope you're having a good start to your week! I'm sending this out having just gotten off the plane from Treefort Music Fest, hence the later timestamp than usual.

This is the second edition of Water & Music's new weekly digest for free subscribers called Extended Play, which focuses on contextualizing music-industry data. As we introduced last week, each issue of Extended Play will put a different piece of music-industry data in context — drawing from official earnings releases, trade reports, third-party surveys and/or our own first-party research at Water & Music. The overarching goal is to use data as a vehicle to keep you up to date not only with the what of music and tech, but also with the why, how and so what, with actionable insights no matter where you are in your career. You can read the first issue of Extended Play, which covered the state of music livestreaming, by clicking here.

I hope you'll find these insights helpful, and encourage you to forward these and future emails to anyone whom you think would enjoy what Water & Music has to offer.

If you're not interested in receiving these digests in the future, please click here to opt out.

Thanks so much for being part of our community! <3

- Cherie

P.S. In case you haven't seen already, we're going to be part of the next cohort of the Seed Club accelerator, which helps communities like ours build out their own social tokens. The first session kicks off tomorrow, and we're super excited to share updates on the accelerator with you over the next several weeks. Stay tuned :)

Extended Play: Just how difficult is it to make a sustainable living from streaming?

Read this article for free on Water & Music's website.

What does it really mean to “make it” as an artist?

This is probably one of the most cliché yet evergreen questions in the music industry, as artists continue to navigate ever-shifting contracts, algorithms, power structures and business models on their path to longevity. It’s also a highly subjective question, as no two artists’ career goals or fan bases look the same.

I’ll pose the argument that “making it” as an artist is more about sustainability than about scale — not about reaching any arbitrary popularity benchmark, but rather just about being able to sustain yourself financially off of doing the creative work that you love. With this framing, we can start to move from subjective to more objective measures — benchmarking artists’ earnings against the costs and standards of living across various markets and taking into consideration the unique challenges that emerging artists face, especially when it comes to the often unpredictable, inconsistent nature of royalty payments and freelance work. This exercise becomes especially relevant against the backdrop of grassroots artists and national governments alike launch in-depth critiques of Spotify and other dominant streaming services, demanding that these platforms pay artists more fairly for the value that their catalogs drive.

So, let’s reframe and refocus the question: What does it really look like for an artist to sustain themselves off of streaming, the largest source of music consumption revenue today?

This leads us to our main data points for this week (emphasis added):

— “Music Creators’ Earnings in the Digital Era,” a 224-page report from the UK Intellectual Property Office (IPO)

Let’s paraphrase: According to the UK IPO, it’s estimated that only around 0.4% of artists on streaming services (1,723 artists) generate enough streams in the UK (1 million streams/month) to make a sustainable living out of music. With some back-of-the-napkin math, this activity amounts to around $3,000–$5,000 a month in streaming royalties from the UK.

As with any research report, these data points come with a bunch of asterisks attached to them. We’re not sure how many streams these top artists generate outside of the UK, since the researchers were only able to work with local consumption data. And there are certainly performing artists out there who are able to make a full-time living without relying on streaming (say, members of symphony orchestras) who are not considered in this calculation. That said, I think the million-monthly-stream threshold is a reasonable place to start, considering the number of team members (or ensemble members) with which a commercially active artist might have to split revenue, the nature of label contracts that take the majority of artists’ royalties and the fact that the UK IPO’s figure does assume the existence of some outside revenue streams.

Plus, there are two asterisks that I think are actually productive for today's discussion. The first one is that the vast majority of streams for the top 0.4% of artists — 65% to 75% of streams to be more precise — are coming from back catalog, not from new music. This range is consistent with MRC Data’s recent claim that 66% of all streaming consumption comes from back catalog, which, as a reminder, consists of songs that are older than 18 months.

|

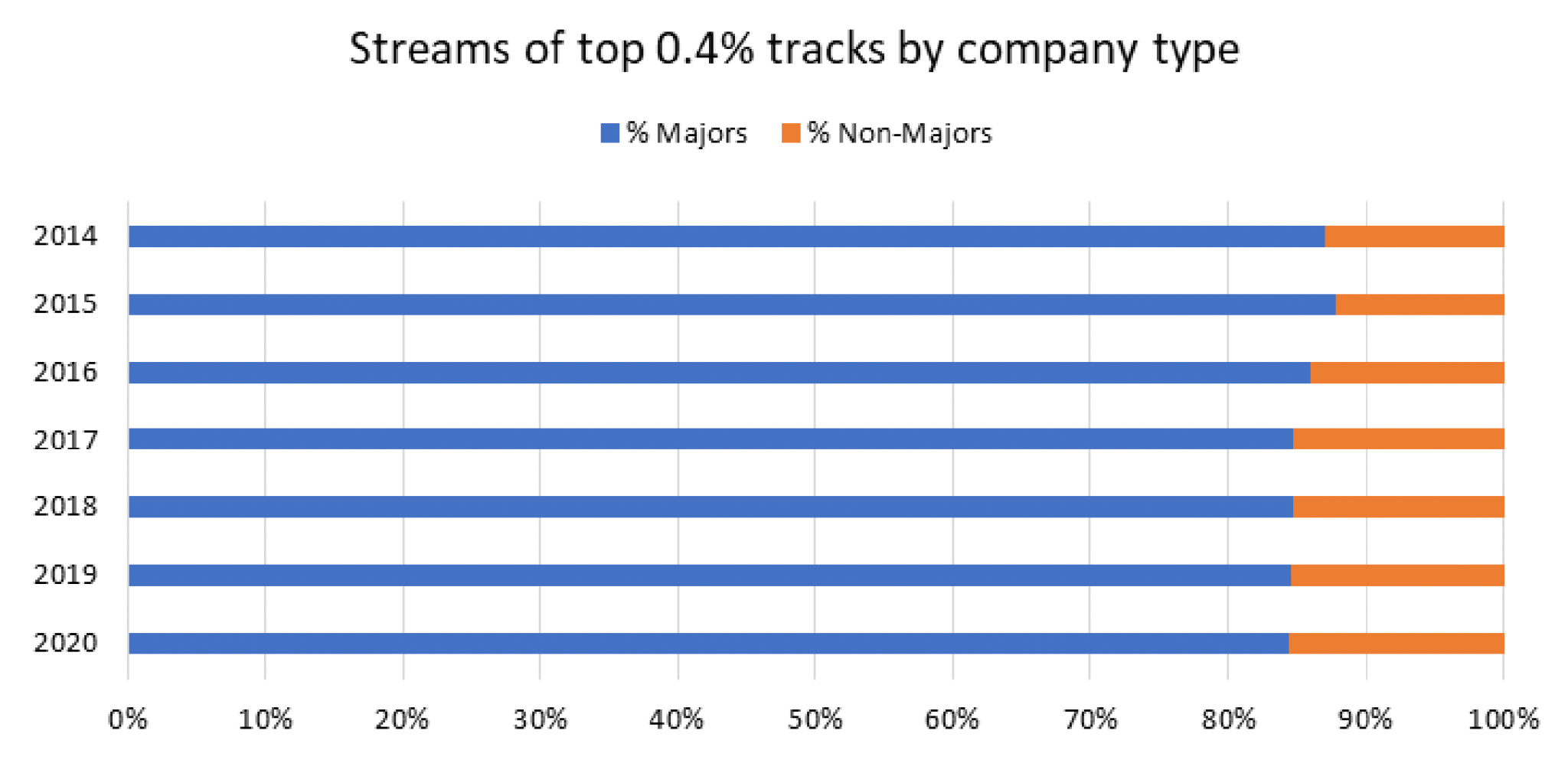

Secondly, the vast majority of these artists in the top 0.4% are likely signed to major labels. According to the same UK IPO report, if we look at the top 0.4% of tracks (not artists) on streaming services, major-label releases have been outperforming non-major releases by a factor of 6 to 1 for the past six years, even as supposedly democratic streaming services have gotten more popular.

|

So, when the UK IPO says that there are 1,700-odd artists whose catalogs generate a million streams a month in the UK, keep in mind:

- Most of these streams are for older releases, so arguably skew away from emerging artists;

- These artists likely have major-label resources that enable them to achieve this streaming threshold, and

- The major-label artist majority in this segment also won’t get access to the lion’s share of revenue generated by those streams, due to the nature of major-label recording contracts.

In other words, the number of independent, unsigned and/or emerging artists who meet the UK IPO’s sustainable streaming threshold is even lower — likely clocking out in the low- to mid-hundreds of artists, if I had to guess.

Look at hard numbers, not just percentages

One general word of wisdom when analyzing data over time is to consider hard numbers and percentage change equally, as just relying on one over the other won’t tell you the whole story. This advice might sound really basic, but it’s always struck me how little music-industry communication follows it, especially when talking about modern prospects for independent artists.

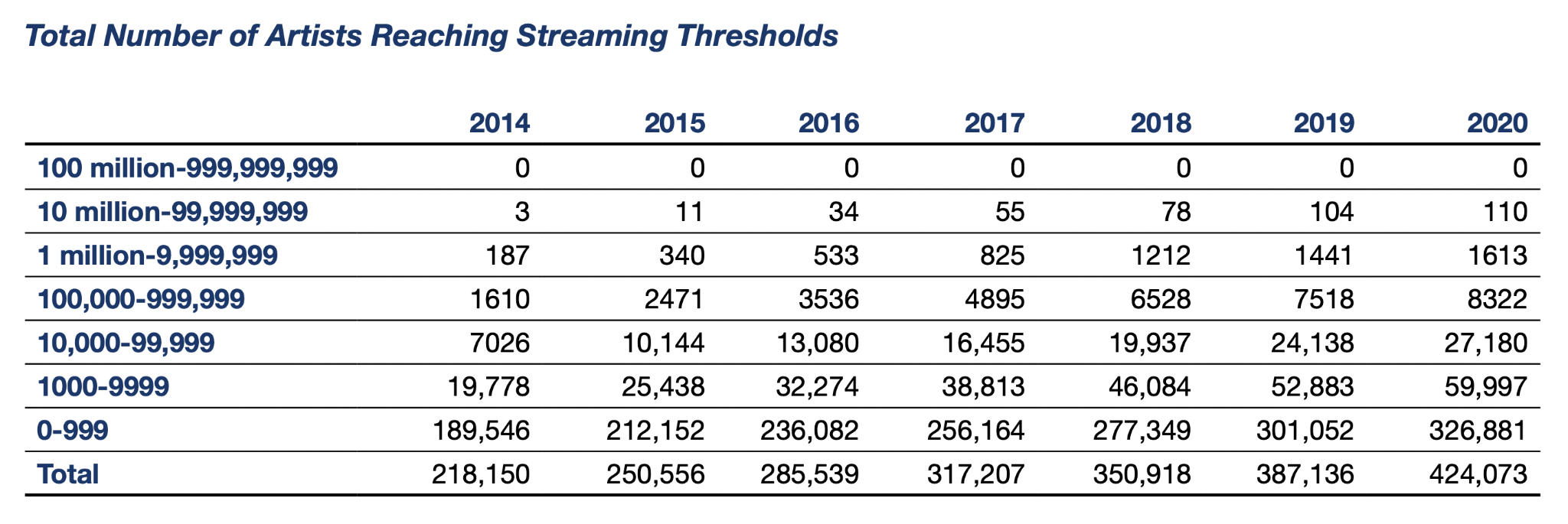

A quick note on methodology: To arrive at its conclusions, the UK IPO partnered with the Official Charts Company (OCC) to gather data on “all streams in a sample ‘month’ corresponding more or less to October in each of the years from 2014 to 2020,” across all services that operate legally in the UK. Based on OCC data, the report’s authors took the entire dataset of artists whose songs have generated at least 1 stream in each year from 2014 to 2020 and broke down that dataset into the following seven streaming thresholds:

|

Looking at the above table, 351 artists generated over a million streams in a sample month in 2015, or 0.1% of the total artist set that year (250,556 artists). In comparison, as established earlier, 1,723 artists generated over a million streams in October 2020, or 0.4% of the total artist set that year (424,073 artists).

Using this data, the following sentences might technically be true:

- Over the past five years, the number of artists who are able to make a sustainable living off of music has increased 5x (351 vs. 1,723).

- Over the past five years, the share of artists able to make a sustainable living off of their music has increased 4x (0.1% vs. 0.4%).

We’ve seen other companies with skin in the game of monetizing independent music publish similar figures that focus on growth. For instance, in a press release last year, AWAL claimed that the number of their roster artists earning over $100,000 in streaming revenue every year “has grown by over 40%.” According to Spotify’s Q1 2021 earnings report, the number of artists on their platform generating more than $50,000/year was up 80% since 2017, the number making more than $100,000/year was up 85% and the group making over $1M/year was up 90%.

But this is a perfect example of a case study where growth certainly doesn’t tell the whole story. Yes, the share of artists able to generate a million streams a month in the UK has quadrupled — but we’re still talking about only 0.4% of artists who are able to achieve this milestone. The streaming game as we know it today is still so disproportionately stacked against artists who don’t have access to major-label resources, or don’t already have an extensive back catalog under their belts.

What DSPs won’t tell you: It’s getting harder

One of my personal revelations reading through the UK IPO report — and what I think is missing from a lot of discussions about what it takes to “make it” in streaming — is that the number of streams an artist needs to make a sustainable living today is significantly higher than it was 5 years ago.

It’s not just that rising competition in the marketplace makes it harder for artists to be heard, or that artists are recording, writing and producing songs in larger teams, splitting their revenue pie into more and more fragments. It’s also that the overall streaming pie is not growing as fast as the number of artists who are releasing new music.

This trend is clearest with market leader Spotify — which continues to pursue growth through its discounted account bundles like its Family Plan and its Hulu/Showtime bundle for students, and has expanded into more international markets where consumers are simply not used to paying for music streaming, especially in Asia, Africa and Latin America. As a result of these initiatives, Spotify’s average revenue per user has declined by nearly 40% between 2015 and 2020, as Glenn Peoples reported for Billboard earlier this year. While Apple Music has claimed that it pays a penny per stream to artists, one can easily see these declining royalty rates happening for other services like Amazon Music, which its parent company is aggressively bundling at a discount with Amazon Echo products.

This in turn pulls down the average per-stream payout rates that artists see in their royalty checks, as an accelerating number of them fight for the share of a pie that can’t keep up. The UK IPO report’s calculations suggest that average per-stream royalty rates in the country have gone down by 50% from 2012 to 2020, from $0.02/stream to $0.01/stream. In other words, a “typical” artist has to generate twice as many streams today as they did in 2012 to earn the same amount of money.

So what, you might ask?

There are two main questions that come to mind. The first, perhaps most obvious one is what, if anything, music streaming platforms should do about this — and how responsible they should be for communicating, let alone remedying, the reality of the situation.

I think a lot of artists’ critiques of the dominant streaming model stem from the fact that it inherently equates sustainability with scale, a correlation made clear by the UK IPO’s report. Not all artists necessarily want to work their asses off to reach millions of listeners; some may care more about fostering deeper community among a smaller group of fans. Platforms like Spotify and Apple Music could start by offering alternative revenue models to artists on-platform — perhaps models that reward diehard fandom, not just passive consumption — so that the barrier to sustainable income is not so high in terms of audience size. Or, recognizing the 99%+ of artists on their platforms who are unable to earn a sustainable living from streaming, these services could create clearer pipelines for emerging artists to get financial support earlier on in their careers when they need it most, even setting up a system for Universal Creative Income as investor Li Jin has suggested recently.

The second question comes more from the perspective of someone like myself who covers music/tech trends — namely, whether the tech startup sector is being honest with itself about the the total addressable market of artist-entrepreneurs who are able to make a substantial income from streaming, let alone a full-time living off of music.

At Water & Music, we’ve been tracking funding rounds for music/tech startups over the past nine months, many of which are building their business case around the assumption that artists’ streaming revenue is growing (e.g. Shodement, which recently raised funding for a tool that gives upfront streaming advances to artists on supposedly better terms than label contracts). But if we’re being realistic, the TAM of artist-customers who are independent and earn enough money from streaming to be comfortable siphoning off part of that money to add-on tech tools on top of their existing distribution stack — let alone enough money to be worth it for startups who are trying to serve them — is likely just a grain of rice in VCs' eyes.

All in all, the UK IPO report presents a compelling picture that will likely drive debates about the future of artists' careers for years to come: While the number of artists in the top 1% (or, in this case, 0.4%) may be growing in absolute terms, it also seems that, due to a lot of factors like declining royalty rates and increasing competition for attention, the climb to get there seems steeper than ever.

More of our coverage on music streaming models:

- How Spotify's new advertising strategy impacts artists

- The music industry's biggest messaging problem

- Why artists are releasing "mood EPs" to game Spotify's algorithm

- Niche music streaming services: Exclusive database

- Music streaming services are losing their brand identity

Click here to opt out of future Extended Play digests.

Water & Music

Research & intelligence for the new music business.

June 19, 2025 HAPPY THURSDAY LAST CHANCE NYC Next Wednesday, we're hosting a one-of-a-kind panel on music tech investment, in partnership with New York Music Month and the Mayor’s Office of Media & Entertainment. We're approaching 90% capacity — we have just 40 spots remaining for what's shaping up to be an exceptional evening connecting leaders and innovators across music, tech, entertainment, and finance. When: Wednesday, June 25 | 6:00–9:00 PMWhere: Perkins Coie LLP | 1155 6th Ave, 22nd...

May 20, 2025 HAPPY TUESDAY MEET US IRL in NYC We're thrilled to announce that Water & Music is teaming up with the NYC Mayor's Office of Media and Entertainment for New York Music Month 2025! This is our second time partnering with this incredible initiative, and we're taking things to a whole new level with not one, but two signature events that celebrate NYC's thriving music tech ecosystem: EVENT #1: NY MUSICTECH MEETUP & DEMOS Monday, June 9 | 6:00–9:00 PMPublic Records | 223 Butler...

March 31, 2025 HAPPY MONDAY new webinar DETAILS Date: Thursday, April 10, 2025 Time: 1PM–2PM EDT Location: Online via Zoom PRICING Current Members: FREE Non-members: $30 RSVP NOW As AI-generated music proliferates, the industry's central question is shifting from "Can AI create music?" to "Who deserves credit and compensation when it does?" Join W&M team members Cherie Hu, Alexander Flores, and Yung Spielburg for a focused 60-minute webinar, where we'll cut through the hype around one of the...