Extended Play: The creator economy is growing much faster than music streaming

Water & Music — The innovator's guide to the music business.

Today's date is November 3, 2021.

Thanks so much for being a paying Water & Music member.

Hello Reader,

Happy Wednesday!

The past few weeks have been a wild journey down the Web3 rabbit hole on our end. We're finalizing W&M's token strategy in the last stretch of the Seed Club accelerator (and gearing up for demo day next week), and I've been running around New York this week for the NFT.NYC conference (read: mostly the parties on the fringes). We also just launched the research process in our members-only Discord server for our next collaborative report on music and crypto — which I'm convinced will be one of the most interesting and valuable resources on the topic this year, with different research sub-threads around generative art, NFT contracts, fan sentiment and more. Super excited for what's in store for our community. :)

Below this note is the latest issue of Extended Play. In case you're new here, Extended Play is our free column focused on contextualizing music-industry data — drawing from official earnings releases, trade reports, third-party surveys and/or our own first-party research at Water & Music. The overarching goal is to use data as a vehicle to keep you up to date not only with the what of music and tech, but also with the why, how and so what, with actionable insights no matter where you are in your career.

I hope you'll find these insights helpful, and encourage you to forward these and future emails to anyone whom you think would enjoy what Water & Music has to offer.

If you're not interested in receiving these digests in the future, please click here to opt out.

Thanks so much for being part of our community! <3

- Cherie

Extended Play: The creator economy is growing much faster than music streaming

Read this article for free on Water & Music's website.

Happy November. We still have around two months left in the year, but we might as well call it now and deem 2021 the “Year of the Creator.”

Sounds cliché, I know. But looking back at industry discussions in the last year, it’s been practically impossible to avoid the term “creator” — which could be loosely defined as anyone who creates something online that someone, somewhere, finds valuable and wants to pay for — as the universal signifier of what’s to come, culturally, technologically and financially. The Information projects that total venture-capital investments in creator-economy startups will reach $5 billion by the end of this year. VC firms like Antler and SignalFire and research/strategy firms like CB Insights, MIDiA Research and Nonfiction/Bodacious have been churning out their own creator economy reports and market maps — the topographies of which could change by the week, given how fast the market is moving.

From the earnings potential of the d’Amelio family to the role that apps like Clubhouse have historically played as watering holes for the Elons and Zucks of the world, there’s understandably a lot of hype around the more public figureheads of the “creator-first” movement. But in my view, there isn’t quite enough focus on the companies that arguably have the most power in this economy: The fintech rails that actually control the flow of creator money.

For all the valid ongoing buzz around areas like crypto and Web3, the reality of today’s situation is that it’s still largely traditional fintech and payment-processing companies like Stripe and PayPal that serve as the pipes making the creator economy go round. And in terms of understanding how the market for creator tech is evolving in a more concrete way — and where, if at all, music-industry business models fit in — payment and fintech companies are data gold mines.

This brings us to our featured data points for this week:

- Edwin Wee, “Indexing the creator economy,” Stripe corporate blog

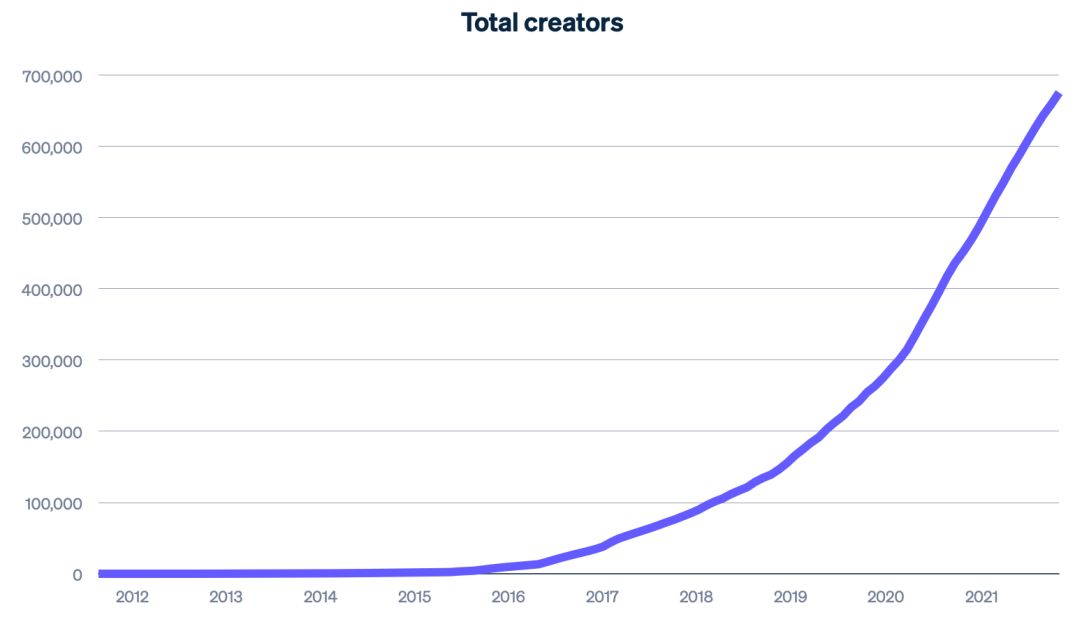

Here’s Stripe’s own graph showing the growth in cumulative creators onboarded over time:

|

There’s a highly strategic reason why Stripe published aggregate creator earnings data: The company is trying to dig itself out of the B2B woodwork and publicly position itself as an ally to the creator class. In the world of tradfi and payment processing, they’re certainly not alone in this strategy. On the exact same day a few weeks ago (Oct. 13), Visa announced a new program to offer creators “consultative services to navigate the world of both crypto and traditional payment infrastructure,” while Cash App (part of the Square family, alongside Tidal) announced the launch of their own creator grant program called Cash App Studio, which will focus on funding creative projects for musicians and other creative professionals. Perhaps this pattern is more reactive to recent controversies like OnlyFans’ temporary ban on sexually explicit videos back in August — which was driven by pressure from credit card companies, and created a PR crisis for the latter group with respect to their ability or willingness to support new generations of creators.

Because this week’s featured data is coming from Stripe’s corporate comms, there are obviously many asterisks in terms of data limitations. For one, we don’t know what the 50 platforms analyzed actually are; nor do we know whether these platforms are actually the top 50 revenue generators for Stripe, or were just handpicked examples for the purpose of driving the company’s core argument about the creator economy’s growth.

There’s also no additional information about how exactly this $9B+ in creator revenue (which Stripe claims will surpass $10B “soon”) is distributed across creators, or over time. In previous installments of Extended Play, I covered the extreme power laws at play in areas like music streaming and livestreaming — whereby the top 1% (or less) of creators consistently command the majority of revenue, fostering the equivalent of a zero-sum-game environment for everyone else. We don’t know what that power law looks like in Stripe’s creator data yet; my hunch is that this $9B is similarly skewed towards the top 1% to 5% of creators.

With all this said, I think Stripe’s findings are still a helpful start for contextualizing the music industry’s role — or lack thereof — in the widening creator-economy conversation, and mapping out tangible ways that artists’ business models will evolve in the coming years.

Music is still an afterthought in the creator economy

What immediately stood out to me from Stripe’s blog post is that the creator economy is growing much more quickly than the music streaming economy right now, by multiple measures.

For instance, while the number of audio creators on Spotify roughly doubled from 2018 to 2021, the overall number of creators using Stripe grew by 8x over the same time period. In terms of revenue, certain subsectors of the creator economy are growing as much as 8x faster as music streaming. According to Stripe, community platforms like Luma have seen a 150% increase in revenue year-over-year in 2021 — far outpacing the 25% year-over-year revenue growth that Spotify reported this quarter, and the 17% year-over-year growth that the IFPI last reported for the entire global music streaming market in 2020.

|

To understand this gap, it’s important to reiterate that music streaming is not part of the “creator economy” by most definitions of the latter term. As I’ve written in the past, some of the core tenets of the creator economy (or “passion economy,” as some investors formerly called it) include defying commodification, enabling direct support from fans or followers and giving creators the ability to charge a price that matches the value they provide, not just the cost of bringing their products to market. The dominant music streaming model as we know it today defies almost all of these points: It encourages the commodification of music via mass aggregation of tens of millions of songs, gives creators no control over their pricing and does not serve as a channel for direct-to-fan engagement period, let alone direct-to-fan payments.

Perhaps for these reasons, music as an industry is usually an afterthought or an asterisk in creator-economy market maps. For instance, SignalFire bundles together musicians, podcasters, writers and illustrators as “others” in their creator-economy framework, which focuses more on creators and YouTube, Instagram and Twitch.

What does this mean for music companies? As Water & Music covered during the height of the pandemic, one of the biggest music-industry mindset shifts that unfolded in 2020 was a prioritization of direct-to-fan revenue models over third-party aggregation models. When you juxtapose sources like the above Stripe data with suggestions elsewhere that only a small fraction of a percentage of artists generate enough streams to make a sustainable living out of music, the case for this direct-to-fan pivot starts to become stronger.

Namely, many of the fastest-growing revenue streams for artists today have nothing to do with monetizing IP, and everything to do with monetizing fandom and direct relationships with people. While music business models might still be an afterthought for the creator economy, creator-economy business models are no longer an afterthought for music.

The underrated opportunity in education

According to Stripe’s blog post, education is the payment company’s top creator-economy category by revenue, with top platforms including Interval, Podia and Teachable. In reading this finding, I realized that while the online education opportunity is certainly being milked in other subjects like fitness, health, productivity and tech, it seems to have been largely ignored (or at least deprioritized) by the mainstream music industry over the past several years. According to our own music/tech investment database, out of the 130 or so music startups that have raised funding so far in 2021, only around 1% are education apps.

There are a handful of potential reasons behind this gap in investment from the music industry — from the amount of time and resources required to craft a high-quality, intimate music learning experience, to the somewhat backwards stereotype that you either “do” or “teach” music but never both. But the pandemic freed up the schedules of performing artists to invest in other creative projects, and also gave everyday people more time to kill at home. As MIDiA Research’s Mark Mulligan recently wrote: “The combination of the catalyzing effect the pandemic had on musicianship and the surge of online learning tools — especially YouTube tutorials and tools like guitar tab apps – is increasing the number of people becoming musicians.” And through the lens of education, the market for creative tools for music starts to look much bigger, far beyond just music creation and distribution software.

As a result, a wide variety of celebrities across genres are pursuing splashier, more public partnerships with music education apps, as a way to promote their own brands of accessibility and relatability while diversifying their digital revenue. Key examples include but are not limited to Charlie Puth’s songwriting course on Monthly, Kimbra’s vocal course on Soundfly, Nas’ series on MasterClass and Metallica’s upcoming course on Yousician.

Hopefully, the ongoing growth in creator-economy platforms — especially around areas like education — will encourage the music industry to think not only about new kinds of revenue streams, but also new, more expansive views of fan bases and “customers” and how technology can best serve them. And by the data we have so far, the business case for new ways of thinking about the music industry’s future growth is getting increasingly futile to ignore.

More of our coverage on music and the creator economy:

- The shape of Web3 music communities: Internet forums with a shared bank account

- Superfan engagement platforms: Track 40+ tools

- The music industry’s biggest messaging problem

- Three parallel futures for social audio

- Is music streaming part of the “passion economy”? It’s complicated

Click here to opt out of future Extended Play digests.

Water & Music

Research & intelligence for the new music business.

June 19, 2025 HAPPY THURSDAY LAST CHANCE NYC Next Wednesday, we're hosting a one-of-a-kind panel on music tech investment, in partnership with New York Music Month and the Mayor’s Office of Media & Entertainment. We're approaching 90% capacity — we have just 40 spots remaining for what's shaping up to be an exceptional evening connecting leaders and innovators across music, tech, entertainment, and finance. When: Wednesday, June 25 | 6:00–9:00 PMWhere: Perkins Coie LLP | 1155 6th Ave, 22nd...

May 20, 2025 HAPPY TUESDAY MEET US IRL in NYC We're thrilled to announce that Water & Music is teaming up with the NYC Mayor's Office of Media and Entertainment for New York Music Month 2025! This is our second time partnering with this incredible initiative, and we're taking things to a whole new level with not one, but two signature events that celebrate NYC's thriving music tech ecosystem: EVENT #1: NY MUSICTECH MEETUP & DEMOS Monday, June 9 | 6:00–9:00 PMPublic Records | 223 Butler...

March 31, 2025 HAPPY MONDAY new webinar DETAILS Date: Thursday, April 10, 2025 Time: 1PM–2PM EDT Location: Online via Zoom PRICING Current Members: FREE Non-members: $30 RSVP NOW As AI-generated music proliferates, the industry's central question is shifting from "Can AI create music?" to "Who deserves credit and compensation when it does?" Join W&M team members Cherie Hu, Alexander Flores, and Yung Spielburg for a focused 60-minute webinar, where we'll cut through the hype around one of the...